Why does automation still feel slow even after insurers invest millions into AI?

Usually, because the workflow still breaks at intake.

A claims model can’t fix incomplete forms, messy PDFs, or customer data buried inside email threads. That’s why many intelligent automation in insurance projects struggle to deliver measurable ROI despite strong technology underneath.

This guide breaks down what actually makes automation work across the full insurance chain: the evolution of insurance automation, the operational bottlenecks that kill performance, the highest-ROI use cases, and how to build an automation roadmap that scales in production.

What intelligent automation in insurance actually means

The standard definition of intelligent automation in insurance is straightforward: a combination of robotic process automation (RPA), artificial intelligence (AI), machine learning (ML), and natural language processing (NLP) used to handle complex insurance processes.

That’s technically correct. An intelligent process automation system combines these technologies to automate manual processes, reduce repetitive tasks, and support better decision-making across the insurance industry.

But that definition starts in the wrong place.

It focuses on internal systems — policy admin, claims management, underwriting engines — and skips the moment that actually determines whether automation succeeds or fails: the first customer interaction.

If your intake layer is messy, incomplete, or unstructured, everything downstream suffers:

- AI models don’t have clean inputs

- Underwriting decisions slow down

- Claims processing times stretch

To understand what intelligent automation insurance really looks like, you need to map the entire flow, not just the backend.

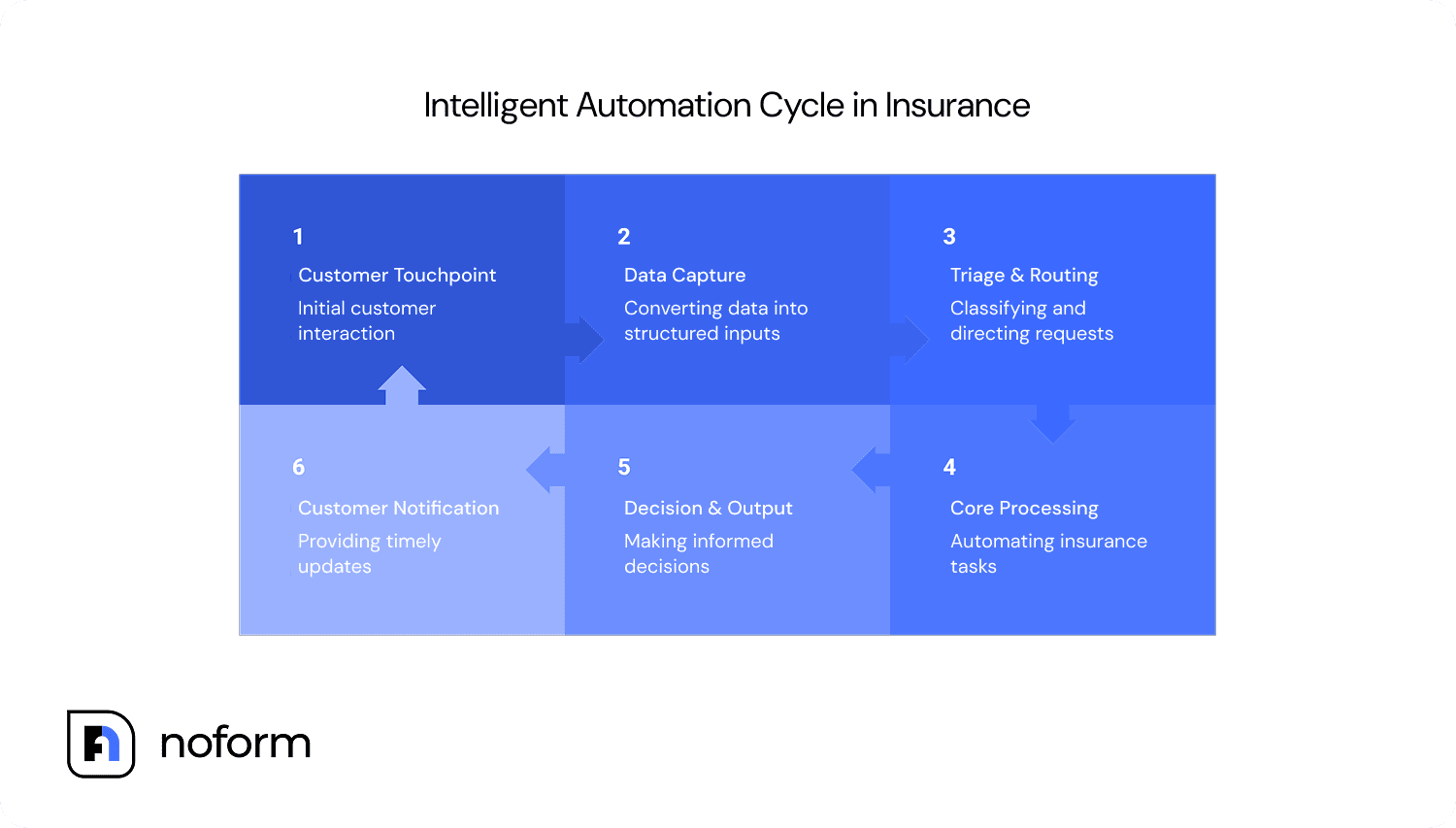

A working model covers the full customer journey:

- Customer touchpoint: Entry points like forms, chat, or conversational AI insurance intake. The starting point for both customer expectations and data quality.

- Data capture: Turning emails, documents, and free text into structured inputs using AI technologies.

- Triage & routing: Classifying requests and directing them to the right workflow to avoid bottlenecks and unnecessary manual tasks.

- Core processing: Policy management, claims data collection, automated claims processing, and automation in underwriting.

- Decision & output: Risk scoring, pricing, and approval, supported by predictive analytics and often a human-in-the-loop for edge cases.

- Customer notification: Clear, fast updates that directly impact customer satisfaction and response times.

This shift is already reshaping the market. The global intelligent automation insurance sector is projected to reach $10.24 billion with a 32.8% CAGR, yet according to Boston Consulting Group, only 7% of insurers have achieved enterprise-wide transformation. Most are still automating disconnected parts of the workflow instead of the full chain.

The pressure increases in August 2026, when EU AI Act insurance compliance requirements begin raising the standard for explainability and audit trails across automated insurance workflows.

“Insurers aren’t losing the AI race because they bought the wrong model. They’re losing it because they fed the right model the wrong data.”

The evolution of insurance automation

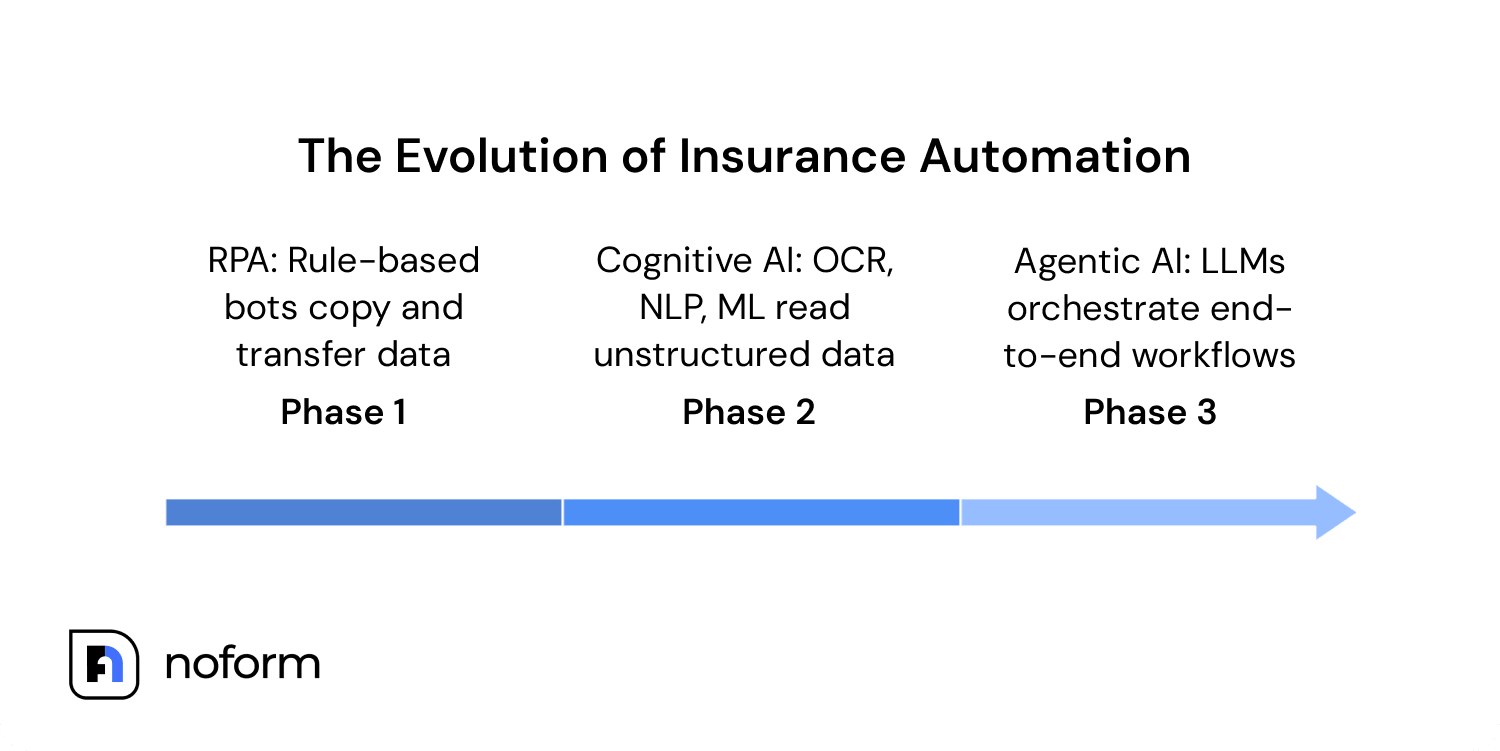

The insurance sector didn’t jump straight into AI-driven workflows. Automation evolved in stages, with each phase solving a different operational problem.

| Phase | Technology | What it does | Core limitation |

| Phase 1 — RPA | Rule-based bots | Copies and transfers structured data between systems | Breaks when processes or formats change; can’t read unstructured content |

| Phase 2 — Cognitive AI | OCR, NLP, ML | Reads emails, PDFs, handwritten notes; extracts meaning from unstructured data | Understands content but cannot orchestrate multi-step decisions independently |

| Phase 3 — Agentic AI | LLMs + orchestration layers | Executes complete workflows end-to-end; makes context-aware decisions; loops in humans only for exceptions | Requires clean, complete input data, which is exactly where most insurers still fail |

Phase 1 — Robotic Process Automation (RPA)

Early automation tools relied on rule-based bots built to move data between systems and handle repetitive back-office work. They improved productivity, but the systems were brittle. Even minor workflow changes could break the process.

Phase 2 — Cognitive AI

The next wave introduced OCR and machine learning capable of reading emails, PDFs, and other unstructured documents. This allowed insurers to automate parts of onboarding, claims review, and policy servicing without relying entirely on manual review. Smarter than basic RPA, but still largely reactive.

Phase 3 — Agentic AI and insurance hyperautomation

The newest generation coordinates entire workflows autonomously. Agentic AI in insurance can verify information, detect fraud, trigger next actions, and support end-to-end claims handling with a human-in-the-loop safety layer. Combined with digital process automation, these systems help insurers adapt quickly as customer behavior and regulatory requirements evolve.

Most carriers already use Phase 2 tools. Very few have reached Phase 3.

The problem starts at intake.

The real problem: Why does the insurance automation chain break?

The biggest barriers to intelligent automation in insurance usually have little to do with the AI models themselves.

The real issues sit deeper:

- Poor intake data

- Fragmented legacy systems

- Operational teams treating AI as a software deployment instead of a business process transformation

That gap explains why many automation projects perform well in demos but struggle in production.

Part 1 — The broken front door

Many insurance firms invest heavily in claims AI, then feed it data collected through a 40-field web form, a scanned PDF, or an email chain that still requires manual data entry.

The result is predictable:

- Customers abandon long mobile forms — complex insurance forms see 60–80% abandonment on mobile

- Underwriters chase missing key information

- Teams correct inputs instead of focusing on meaningful work

According to Deloitte, incomplete intake can add three to five business days per case.

Even highly accurate AI systems struggle when FNOL data arrives incomplete or inconsistent. So while insurers try to automate the entire workflow, the process still breaks at intake.

“Garbage in, garbage out — at enterprise scale.”

|

Three intake patterns consistently break the chain before automation even begins:

|

Part 2 — The palimpsest problem (legacy infrastructure)

A palimpsest is a manuscript where new writing is layered over old text that was never fully erased. The same thing happens inside many insurance company systems.

Modern AI tools are often stacked on top of legacy infrastructure that was never designed to work together. A chatbot connects to an outdated claims platform. An underwriting assistant pulls data from systems that can’t share information cleanly.

Around 42% of insurance documents remain unstructured or semi-structured, while agentic systems require simultaneous access to claims, billing, CRM, and policy platforms. Many legacy systems still lack usable API layers, making connected automation difficult from the start.

Part 3 — The structural barriers that keep carriers stuck

Poor data quality continues to derail automation efforts across the insurance sector. Around 85% of AI projects fail because of poor data quality once pilot models encounter messy real-world inputs.

But technology is only part of the issue.

Boston Consulting Group describes AI transformation through its 10–20–70 principle: only 10% depends on the models themselves. Most success comes from people, process, and operational culture.

As Artem Gonchakov explains:

“Most carriers have AI projects. Few have an AI strategy. The difference determines whether AI produces scattered productivity gains or compounding competitive advantages.”

That gap helps explain why many insurers still struggle to leverage automation beyond isolated pilots. According to RaiseSummit’s 2026 research, 95% of generative AI pilots in 2025 failed to impact P&L.

6 high-ROI use cases across the full insurance chain

The strongest insurance automation ROI comes from connecting the workflow end-to-end instead of automating isolated tasks. The biggest gains usually happen in the handoffs: intake to underwriting, underwriting to claims, claims to compliance.

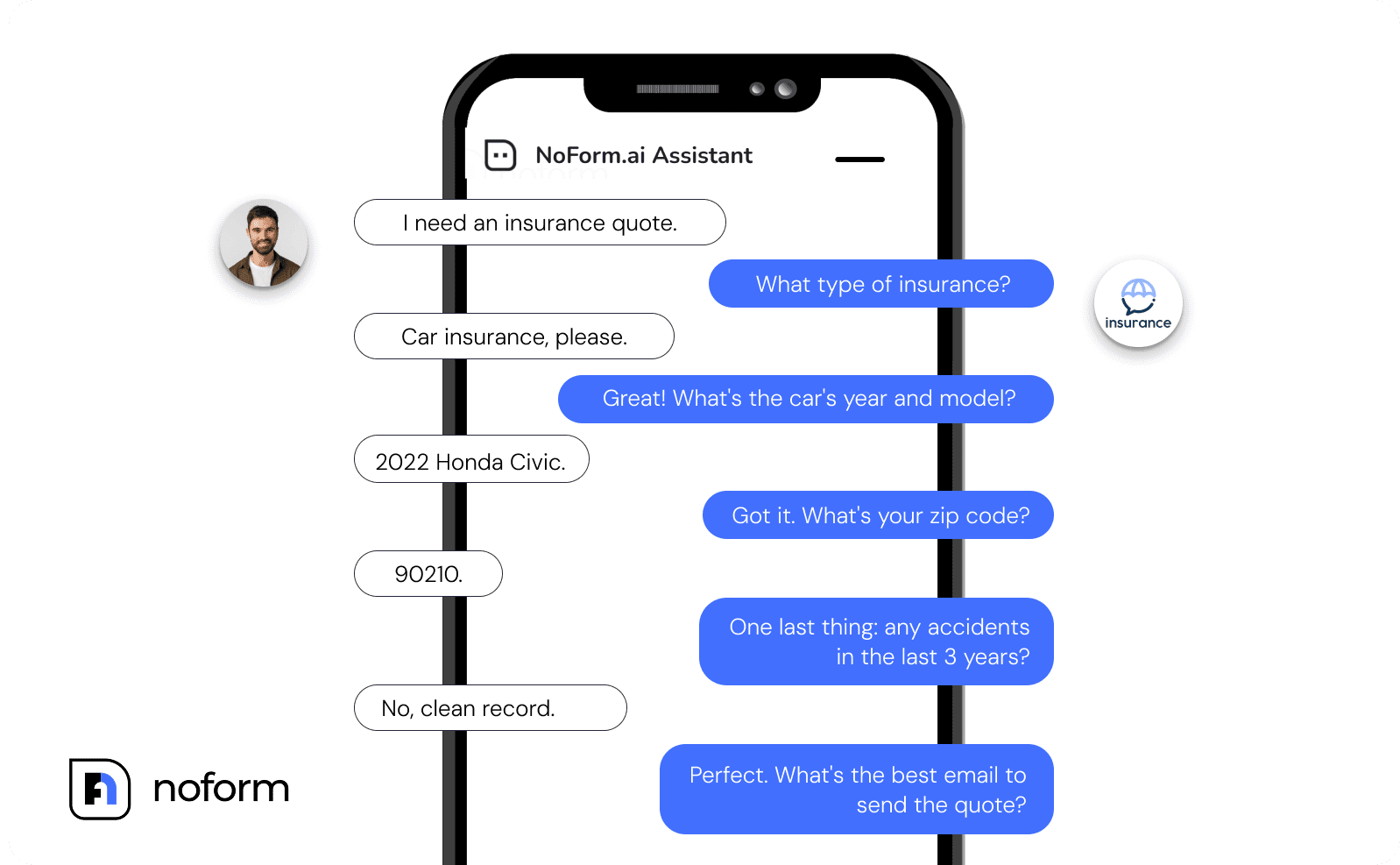

1. Intelligent lead capture & quote intake

Quote workflows usually fail before underwriting even begins.

Static quote forms create drop-offs, incomplete submissions, and underwriting delays before the workflow even begins. Conversational AI changes the process entirely by guiding customers through adaptive, real-time conversations across web, chat, and mobile.

That improves both speed and data quality:

- Up to 55% more high-quality leads

- 38% less underwriting back-and-forth

- 30% faster approvals

NoForm AI acts as a conversational intake layer for insurers, helping automate quote requests while syncing data directly into existing CRM and AMS systems. NoForm AI focuses on the intake stage: capturing the information needed to start a quote or inquiry.

ROI: 3–6 months. No large-scale IT rollout required.

2. Automated underwriting

Traditional underwriting reviews static snapshots. Modern AI models evaluate live risk signals continuously: telematics, weather data, behavioral patterns, and credit indicators.

According to Deloitte, AI-driven underwriting reduced turnaround times from 3.8 days to under 10 minutes. Human reviewers stay involved mainly for edge cases and compliance checks.

ROI: Up to 97% faster turnaround times and significantly fewer routine tasks.

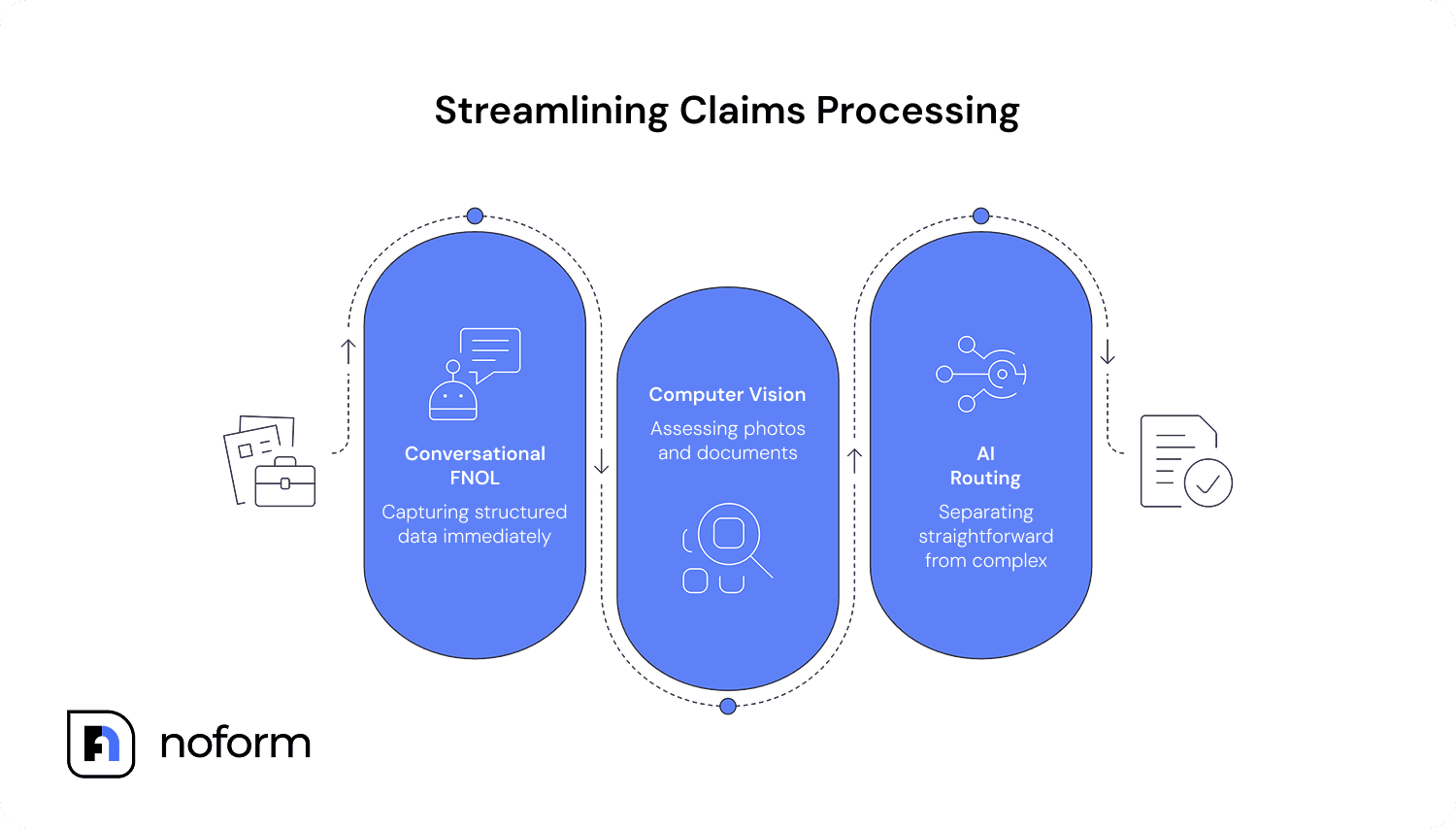

3. Claims triage & FNOL

Claims teams lose enormous amounts of time reconstructing incomplete information after FNOL.

Conversational FNOL captures structured data immediately, while computer vision tools assess uploaded photos and documents automatically. AI routing then separates straightforward claims from cases requiring specialist review.

The impact is substantial:

- Settlement times reduced by 45%+

- Claims resolution reduced from 30 days to 7.5 days in some deployments

ROI: Faster payouts and more adjuster capacity for complex claims.

4. Fraud detection

Human reviewers struggle to detect fraud patterns at scale. Machine learning systems don’t.

Modern fraud engines analyze intake behavior, claims anomalies, document inconsistencies, and relationship patterns simultaneously — often before payouts happen.

That matters in an industry losing more than $40 billion annually to non-health insurance fraud in the US alone, according to the Federal Bureau of Investigation.

Research from Convin found that graph-based AI improved fraud detection accuracy by more than 45%.

ROI: Up to 30% lower fraud-related payouts.

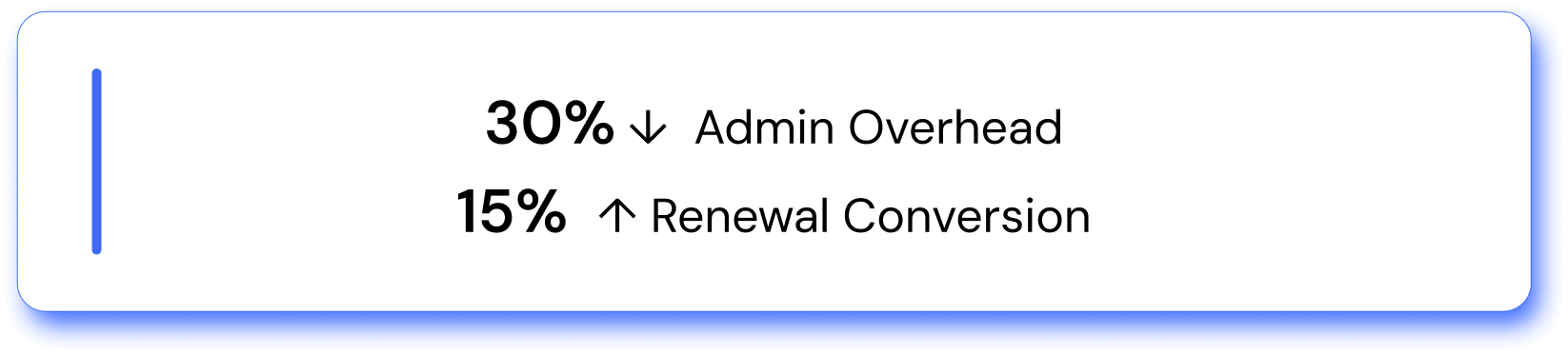

5. Policy administration & churn prevention

A surprising amount of policy administration still revolves around manual follow-ups, renewal reminders, and servicing requests.

Automation removes much of that operational drag. AI systems can trigger renewal outreach automatically, personalize customer communication, and flag churn risks before policies lapse.

Several 2025 deployments reported:

- Roughly 30% lower admin overhead

- 15%+ increases in renewal conversion

ROI: Lower churn, higher customer lifetime value, no additional headcount.

6. Compliance & audit trail

As insurers expand automation uses, compliance increasingly becomes part of the workflow itself.

Modern systems automatically log model versions, confidence scores, approval paths, and decision history — increasingly critical under the EU AI Act, GDPR, and Solvency II.

Automated QA workflows also achieved 95% audit adherence and 65% fewer review errors compared to sampling-based oversight.

ROI: Lower compliance overhead and reduced regulatory exposure.

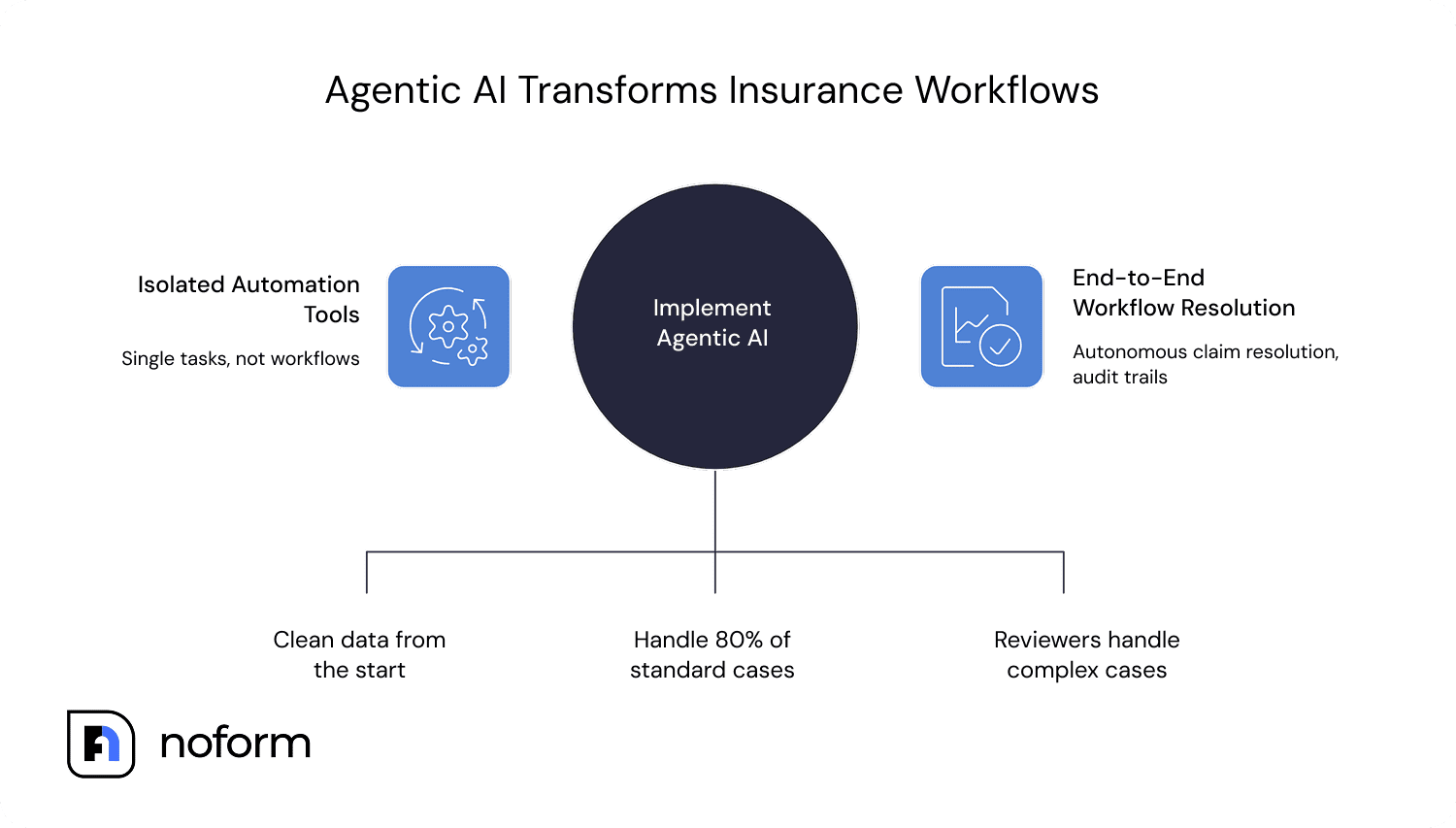

What is agentic AI in insurance, and why does it change the game?

The use cases above all point toward the same shift: insurers are moving beyond isolated automation tools and toward systems that can manage entire workflows autonomously.

In simple terms, agentic AI can pursue a goal across multiple steps instead of completing a single task.

The progression looks like this:

- RPA: Task-level — moving data between systems.

- Cognitive AI: Document-level — reading emails, PDFs, and claims files.

- Agentic AI: Goal-level — resolving a claim or completing a renewal workflow end-to-end.

That changes how insurance teams operate.

In most deployments, agentic systems handle roughly 80% of standard cases automatically, while humans focus on exceptions and judgment calls. By the time a case reaches a reviewer, the AI has already assembled the supporting documents, risk signals, and workflow history.

Gartner predicts agentic AI will autonomously resolve 80% of common customer service issues by 2029.

But autonomy raises the stakes.

Starting in August 2026, the EU AI Act requires auditable trails for automated decisions, while liability remains with the insurer, not the vendor.

That makes structured data flow mission-critical. Agentic systems can only operate reliably when information enters the workflow cleanly from the start.

|

Here’s how that looks in practice, from first contact to resolution:

|

How to build an intelligent automation roadmap for your insurance operation

Insurance companies looking for real automation benefits often invest in back-end AI before stabilizing the workflow itself.

But that approach rarely improves efficiency for long.

Successful intelligent automation insurance implementation starts before any software purchase.

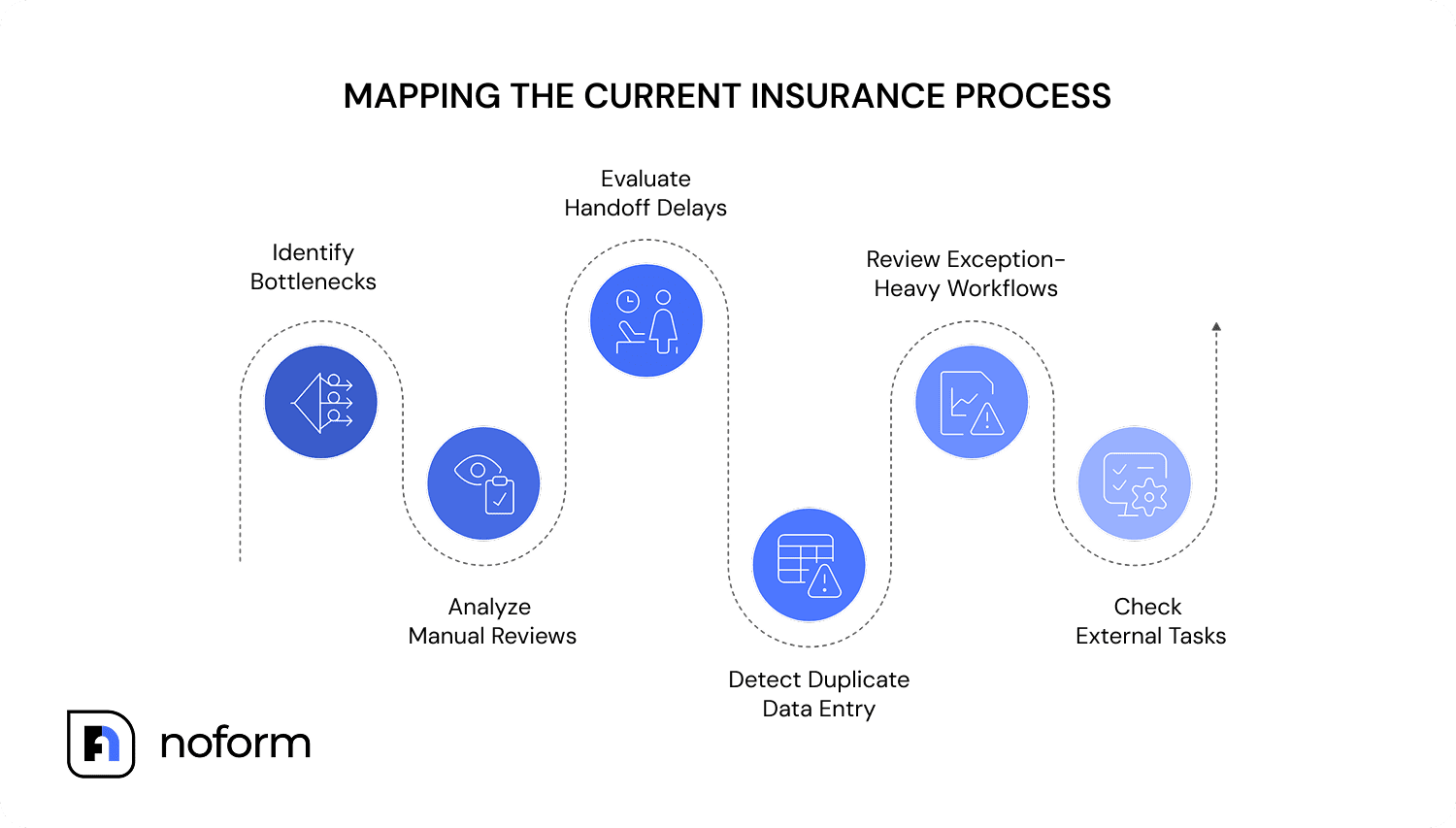

Step 1: Map the current process

Start with process mining across underwriting, claims, servicing, and renewals. The first goal is identifying bottlenecks and inefficiencies before automating anything.

Look for:

- Repeated manual reviews

- Delays between handoffs

- Duplicate data entry

- Exception-heavy workflows

- Tasks completed outside core systems

This shows where time, accuracy, and operational capacity are being lost.

Step 2: Fix intake before anything else

To overcome the automation problem associated with incomplete intake, replace static forms, PDFs, and email-based submissions with structured conversational intake where possible.

Add real-time validation at the point of submission so missing information gets corrected before entering the workflow.

Tip: For MGAs and smaller carriers, this is often the highest-ROI starting point. Many teams improve lead quality and response times within weeks simply by connecting conversational intake tools to their existing AMS through APIs.

Step 3: Structure incoming data automatically

Use Intelligent Document Processing (IDP) to extract data from emails, PDFs, claims files, and attachments automatically. Then layer routing logic on top:

- Low-risk cases move automatically

- Complex claims escalate to specialists

- Missing information triggers follow-up workflows immediately

Tip: API orchestration and middleware can connect these workflows to legacy systems without replacing the core infrastructure.

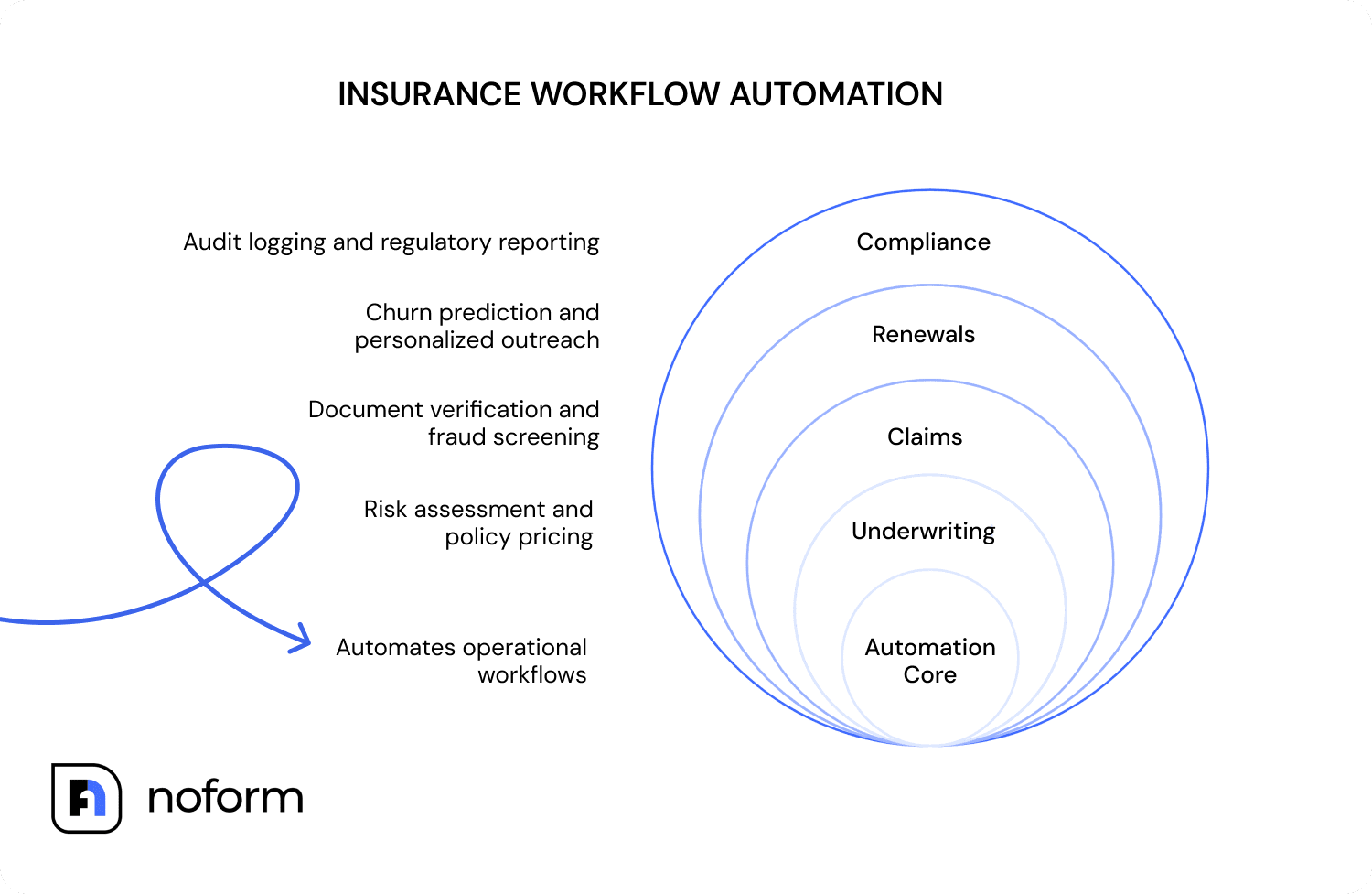

Step 4: Automate core workflows

With intake, routing, and data quality stabilized, automation can expand into the operational core of the insurance workflow:

- Underwriting: Risk scoring, document review, policy checks, pricing recommendations

- Claims: FNOL routing, document verification, fraud screening, settlement recommendations

- Renewals: Churn prediction, renewal reminders, personalized outreach, policy updates

- Compliance: Audit logging, document tracking, approval history, regulatory reporting

👉🏻 Learn more about insurance claims chatbots — how they work, what their benefits are, and how to create one for your business — in our guide.

Most insurers deploy a Human-in-the-Loop (HITL) model at this stage:

- AI recommends actions

- Humans review and approve decisions

- Autonomy expands gradually as trust builds

Step 5: Add governance

Unless both are built together, automation scales faster than governance. So, before expanding beyond isolated workflows, insurers need clear oversight mechanisms in place:

- Human review checkpoints

- Audit logging

- Model monitoring

- Compliance controls

Under the EU AI Act, automated underwriting decisions require auditable documentation showing how the outcome was generated.

Tip: Legal, IT, HR, and compliance teams should be involved early, not brought in after deployment.

Real-world results: what full-chain automation looks like in practice

Building a connected automation workflow does take time and effort. It requires process redesign, staff training, governance, and cleaner data foundations.

But the operational payoff becomes visible surprisingly fast once workflows stabilize.

According to McKinsey & Company, Aviva deployed more than 80 AI models across its operations, reducing liability assessment times by 23 days, cutting complaints by 65%, and increasing NPS sevenfold. The company also invested 40,000 hours into employee training alongside the rollout.

Allianz Partners took an even more aggressive approach. According to RaiseSummit’s 2026 research, the company skipped the pilot phase entirely and launched autonomous automation directly into production across UK and DACH markets in late 2025.

How to choose the right intelligent automation vendor

The insurers seeing real results from automation usually have one thing in common: they chose vendors that could support operational change, not just sell another AI demo.

Before signing, ask five questions:

| Question | Why ask |

| Does your platform handle the intake layer, or only post-submission workflows? | Many systems automate downstream tasks while ignoring where the data quality problem actually starts. |

| How does your system integrate with our existing core policy admin platform via API? | If integration depends on manual workarounds, the automation gap usually returns later. |

| What does your explainability and audit trail output look like for regulatory review? | Insurers need clear documentation to stay compliant under the EU AI Act and other regulatory frameworks. |

| Can you show a production deployment — not a pilot — at a carrier of our size? | A successful proof-of-concept says very little about operational scalability. |

| What does your MLOps framework look like for ongoing model monitoring and retraining? | Models degrade over time. Vendors should already have a process for monitoring accuracy, drift, and performance. |

When comparing your options, watch out for the following red flags:

- No measurable P&L impact from production deployments

- Case studies limited to pilots or innovation labs

- No clear answer around EU AI Act compliance documentation

- Heavy customization required for basic integrations

The strongest vendors usually talk less about the model itself and more about workflow reliability, governance, and operational outcomes.

Conclusion

The biggest gains from intelligent automation happen when insurers treat intake, processing, decision-making, and compliance as one connected workflow instead of separate systems competing for clean data.

And the strongest automation strategies usually start small: fix the front door, stabilize the workflow, then expand gradually once the process becomes reliable.

If you want to see what that looks like in practice, try building an AI assistant with NoForm AI or book a demo to explore how conversational intake can fit into your existing insurance workflow.

Frequently Asked Questions

What is intelligent automation in insurance?

Intelligent automation in insurance combines robotic process automation (RPA), artificial intelligence (AI), machine learning (ML), and natural language processing (NLP) to execute complex insurance workflows, from customer intake and underwriting through claims processing, fraud detection, and compliance logging with minimal human intervention. Unlike basic RPA, it handles unstructured data, adapts to exceptions, and improves accuracy over time. The AI-in-insurance market is projected to reach $10.24 billion, growing at 32.8% CAGR.

How is intelligent automation different from standard RPA?

Standard RPA uses rule-based bots to move data between systems. While fast, it is highly brittle—any minor workflow change can break it. Intelligent automation adds AI and machine learning, allowing systems to read unstructured documents, learn from patterns, and handle exceptions. The most advanced form, agentic AI, goes even further by pursuing multi-step goals like resolving a claim end-to-end without requiring step-by-step human instructions.

Which insurance processes should be automated first?

Start with intake: replace static quote forms and FNOL PDFs with conversational AI. This is the fastest-payback stage (3–6 months) and improves data quality for every downstream process. Then move to triage and routing, followed by underwriting and core claims processing. Fixing data quality at the source before investing in advanced back-end AI is what separates successful deployments from failed pilots.

What ROI can insurers expect from intelligent automation?

Full-chain intelligent automation delivers 30–40% operational cost savings, a 75% reduction in claims resolution time (from 30 days to 7.5 days), and 45%+ faster settlements. Customer service costs can drop from $8–15 per phone interaction to under $1 per AI interaction. Front-end intake automation alone typically generates positive ROI within 3–6 months through improved lead quality and reduced manual data entry.

What is agentic AI in insurance?

Agentic AI refers to autonomous systems that execute entire multi-step workflows independently, receiving a first notice of loss (FNOL), gathering evidence, assessing coverage, detecting fraud, and initiating payment, making contextual decisions at each step without human intervention for qualifying cases. Unlike RPA (single tasks) or cognitive AI (document reading), agentic AI orchestrates decisions across connected systems. By late 2026, over 35% of insurers are expected to deploy agentic AI across at least three core business functions.

What is a human-in-the-loop model in insurance automation?

Human-in-the-loop (HITL) keeps humans in the decision chain for cases requiring judgment or regulatory oversight. In most deployments, AI handles 80% of routine cases automatically and routes the remaining 20% to human reviewers, with a pre-built evidence package already assembled. This satisfies EU AI Act explainability requirements and lets insurers expand AI autonomy gradually as trust is established.