Insurance is one of the few industries where customers spend years hoping they never need the product they’ve purchased. When they finally do, the experience often matters as much as the policy itself. A confusing claim, an unanswered question, or a delayed response can outweigh years of otherwise uneventful service. That’s what makes insurance customer experience such a high-stakes challenge.

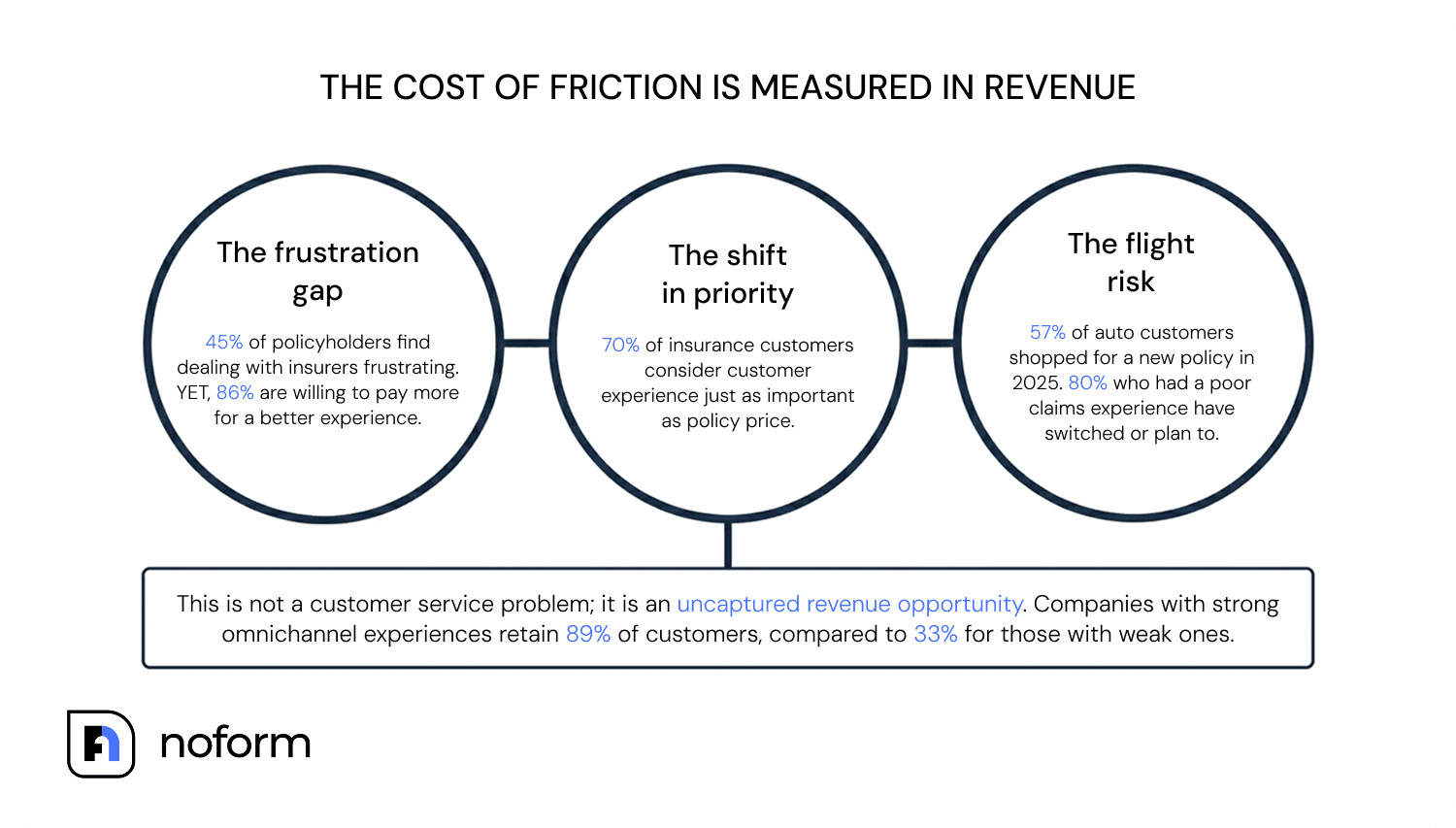

The numbers reflect that reality. While 84% of customers say the experience a company provides is as important as its products or services, and 86% are willing to pay more for better CX, 45% still find dealing with insurers frustrating. That gap has become a business risk.

In this guide, we’ll explore how to enhance customer experience in insurance, from core CX principles and best practices to the trends shaping the industry in 2026.

What is customer experience in insurance?

Customer experience in insurance is the sum of every interaction a policyholder has with an insurer, from researching insurance products and buying coverage to managing policies, contacting support, and filing claims.

On paper, that sounds similar to customer experience in any industry. The reality is very different.

Retail brands interact with customers constantly. Banks may see dozens of interactions per customer every year through mobile apps, payments, transfers, and account management. Insurance companies, on the other hand, often get only one or two meaningful interactions annually.

This creates the defining challenge of the insurance CX: a low-touch, high-stakes relationship.

Customers rarely contact their insurance provider because something good happened. Instead, they reach out after a car accident, a medical emergency, property damage, or another stressful event. As a result, every interaction carries far more emotional weight than a typical retail transaction.

This is why the concept of a “moment of truth” is so important in the customer experience insurance industry. A policyholder doesn’t truly evaluate an insurer when buying a policy. The real evaluation happens when they need help.

Because of this, the strongest insurance CX strategies are built on three pillars:

- Clarity: Easy-to-understand coverage details, transparent communication, and plain-language policy terms.

- Speed: Fast responses, efficient claim processing, seamless digital channels, and convenient self-service tools.

- Trust: Reliable support, consistent communication, and access to human assistance when customers need it most.

When insurance companies get these three elements right, they improve customer satisfaction, strengthen customer relationships, and build long-term loyalty.

Why does customer experience matter in the insurance industry?

The impact shows up in four areas:

It helps insurers stand out from the crowd

Many insurance companies offer similar coverage, similar pricing, and similar policy features. When the products themselves look alike, customer experience often becomes the deciding factor. According to McKinsey, 70% of insurance customers consider customer experience just as important as policy price when choosing an insurer. That’s a significant shift in itself, but customer experience is also becoming a brand factor: user experience now ranks nearly as high as brand in the decision-making process. Fast support, clear communication, and a seamless digital experience can therefore become powerful competitive advantages.

It strengthens customer retention

Research shows that one in three consumers would leave a business after a single negative experience. In insurance, that isn’t an empty threat. J.D. Power found that 80% of auto insurance customers who had a poor claims experience have already switched insurers or plan to. The wider market points in the same direction: 57% of auto insurance customers shopped for a new policy in 2025, the highest shopping rate ever recorded. On the flip side, companies with strong omnichannel customer experience strategies retain 89% of customers, compared to just 33% for those with weak omnichannel experiences.

It helps meet changing customer expectations

Today’s policyholders are comfortable researching coverage, comparing options, and buying insurance on their own. In fact, 47% of auto insurance buyers now purchase through digital channels, compared to 35% through agents and 17% through call centers. Customers are increasingly looking for self-service tools, fast answers, and frictionless experiences across channels.

It drives business growth

Insurers are seeing the financial impact firsthand: 62% of insurance companies report positive ROI from investments in customer experience and digital transformation initiatives.

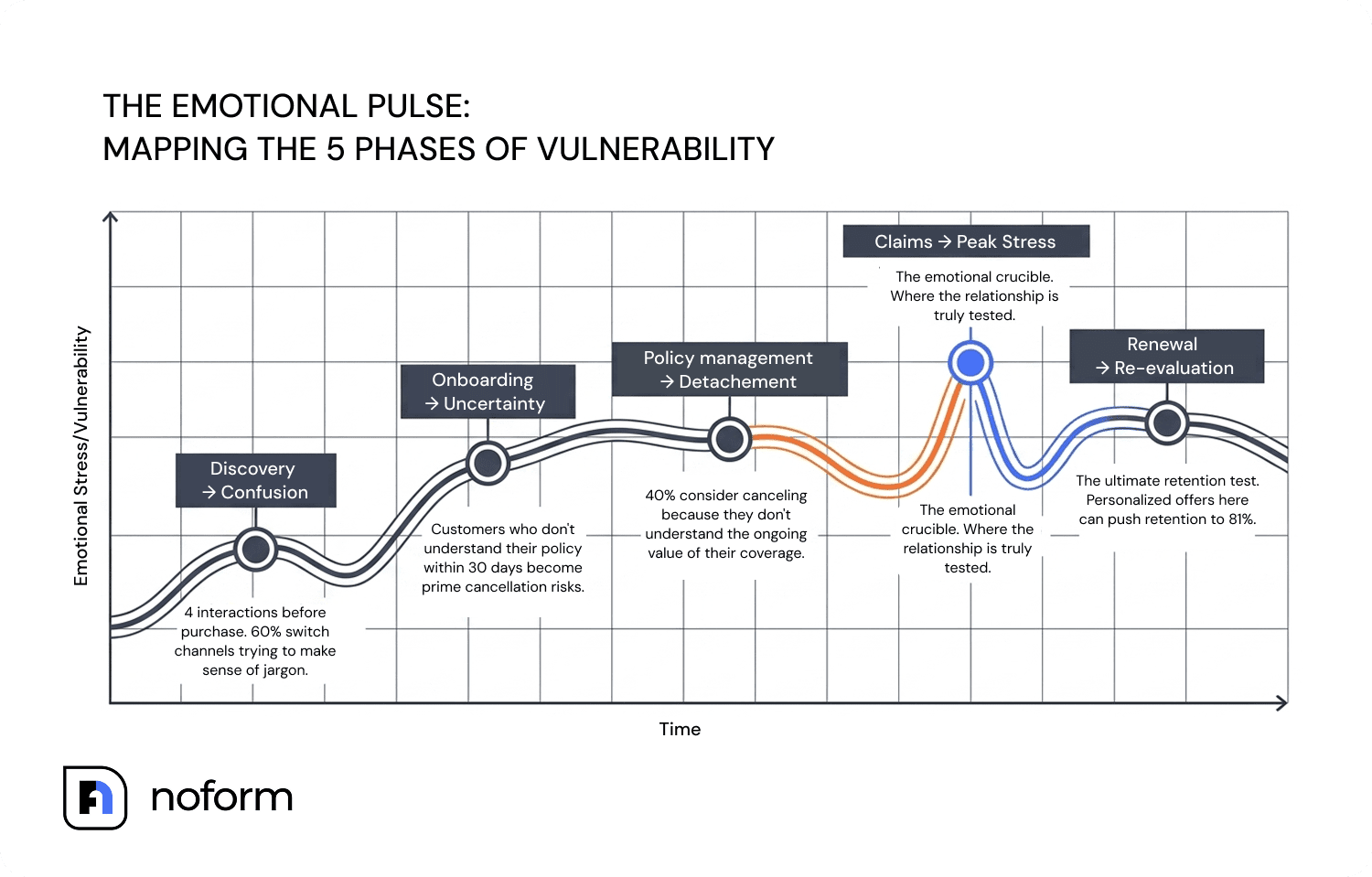

The 5 emotional touchpoints of the insurance customer journey

Most discussions about CX in insurance focus on processes, channels, and technology. Customers experience it differently. What they remember are the emotions attached to each stage of the insurance policyholder journey.

Touchpoint 1 — Discovery (Confusion)

The journey begins with questions. Customers weigh coverage, exclusions, deductibles, pricing, and policy terms across multiple providers, often without a clear way to tell which option best fits their needs. On average, prospects contact insurers four times before purchasing, and 60% switch channels during the process.

The challenge is making sense of it all. Too much information, inconsistent messaging, and insurance jargon can make informed decisions difficult.

To help customers compare options with greater confidence, opt for plain-language policy summaries, side-by-side comparison tools, jargon glossaries, and proactive chat support instead.

Touchpoint 2 — Onboarding (Uncertainty)

The purchase is complete, but many customers still aren’t sure what happens next. They may not fully understand their coverage, how to access benefits, or who to contact if they need help. Customers who don’t understand their policy within the first 30 days are significantly more likely to cancel.

To remove that uncertainty before it turns into frustration, you need a strong onboarding experience. Personalized welcome sequences, a dedicated point of contact, and automated policy explainers can help customers understand their coverage and get value from it sooner.

Touchpoint 3 — Policy Management (Detachment)

Low engagement between major events erodes perceived value over time. In fact, around 40% of policyholders say they don’t fully understand the value their coverage provides and have considered canceling because of it.

To keep the relationship strong and present, offer proactive annual value summaries and regular risk-prevention tips tailored to the policyholder’s profile. You can also consider investing in self-service mobile portals.

Touchpoint 4 — Claims (Stress and Vulnerability)

Reaching this stage is often peak stress for customers. They’re dealing with an accident, illness, loss, or another unexpected event while waiting for answers from their insurer.

This is also where communication gaps become most visible. While 84% of policyholders expect real-time claim updates, insurers provide them only 22% of the time. As a result, 31% have canceled coverage after a poor claims experience, while 64% say they’d switch insurers for better claim visibility.

In order to reduce uncertainty and help customers feel supported during a difficult time, insurers can offer digital claim submission, automated status notifications, and empathetic agent support throughout the process.

Touchpoint 5 — Renewal (Re-evaluation)

As the renewal date approaches, customers start reassessing their options. They compare prices, review coverage, and decide whether staying with their current insurer still makes sense.

For many insurers, this is the first real retention test. Personalized renewal packages, loyalty rewards, and proactive outreach 60–90 days before renewal help reinforce the value of staying. Stats say that insurers that personalize renewal offers achieve retention rates as high as 81%.

What are the biggest customer experience challenges in insurance today?

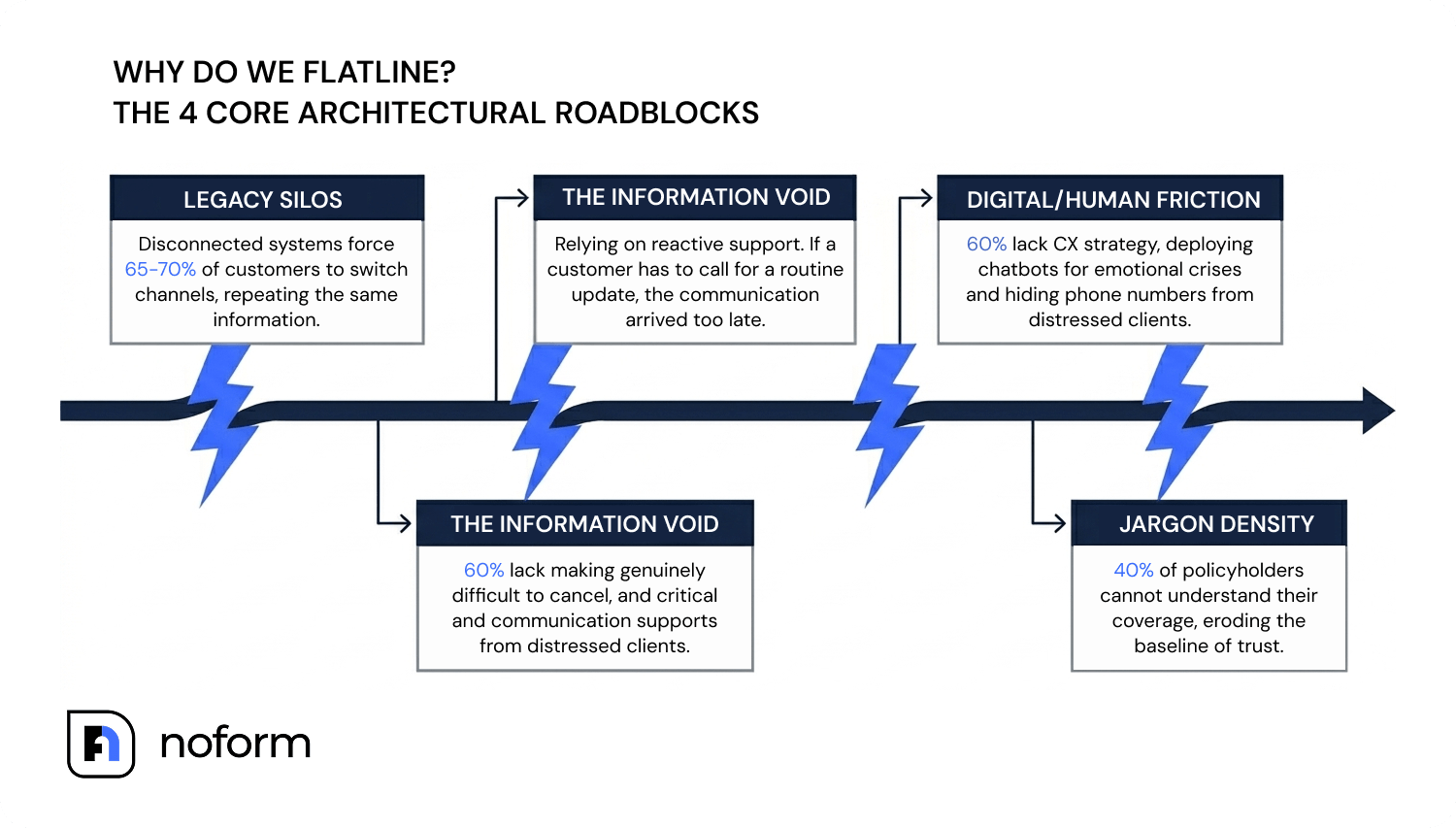

Most insurers understand the importance of customer experience in insurance. The challenge is delivering it consistently. According to IBM research, 42% of customers don’t fully trust their insurer, while 60% of insurers say they lack a clear CX strategy.

Legacy systems & silos

Many insurers still rely on disconnected systems. McKinsey identifies core system modernization as the industry’s top operational challenge, and 75% of insurers plan new technology adoption. In the meantime, customers are often left repeating the same information every time they switch channels.

Claims communication gaps

Claims remain one of the biggest friction points in the customer experience insurance industry. When customers don’t know what’s happening with their claim, follow-up inquiries increase, driving service costs up and trust down.

The human vs. digital tension

Different moments call for different types of support. While 81% of customers prefer self-service for routine tasks, 54% still trust human advisors for complex decisions. Meeting both expectations requires more advanced hybrid models.

Complex jargon

40% of policyholders still struggle to understand coverage and policy terms. Complex language creates confusion and can undermine trust.

How to improve customer experience in insurance: Best practices for insurance CX

Understanding the challenges is only the first step. Enhancing customer experience in insurance requires deliberate changes across the entire customer journey, from the first website visit to policy renewal and beyond.

The strongest customer experience for insurance strategies focus on reducing friction before customers ever feel it.

Modernize claims specifically

Claims are often the most important interaction a policyholder will ever have with an insurer.

Long wait times, unclear next steps, and requests for missing documents can quickly turn a stressful situation into a frustrating one. Any meaningful insurance claims experience improvement should make the process faster, clearer, and easier to navigate.

Priority areas include:

- Digital claim submission

- Automated status notifications

- Clear documentation checklists

Map the full journey, not just the claim

While claims may be the most visible touchpoint, they aren’t the only one that matters. Discovery, onboarding, policy management, claims, and renewal all shape the customer experience.

Before investing in new technology, map all five emotional touchpoints and identify where customers struggle.

Build mobile-first self-service

For many policyholders, the most important channel is already in their pocket. More than 70% access insurance services on mobile devices, making the smartphone the primary insurance portal for many customers.

Audit your mobile experience around the tasks customers complete most often:

- File a claim

- Upload supporting documents

- Check claim status

- Update policy information

Tip: Test these journeys during stressful situations, not ideal conditions.

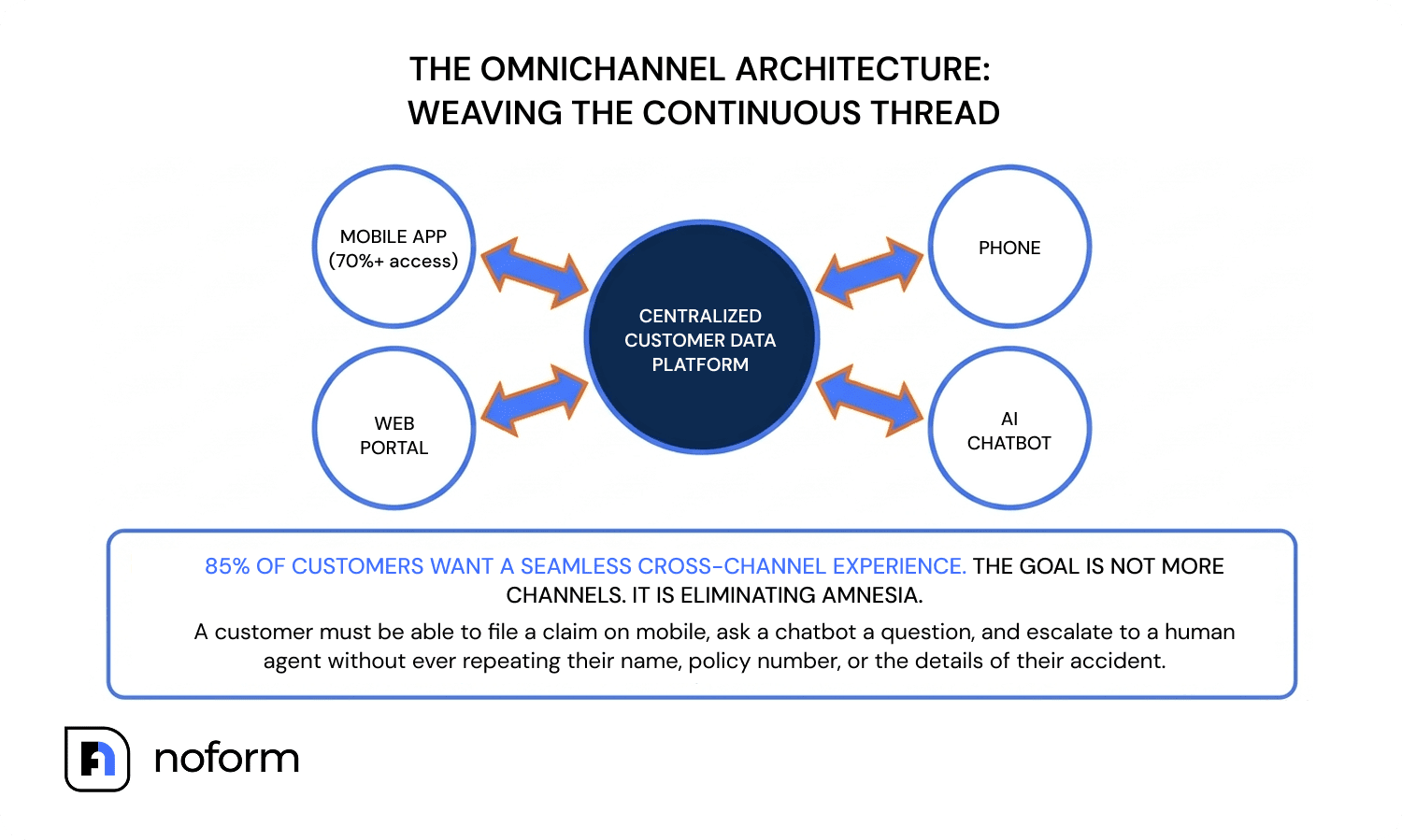

Implement omnichannel without silos

Research shows that 85% of insurance customers want a seamless experience across channels, while more than 70% specifically value smooth omnichannel journeys.

But adding more channels doesn’t automatically create a better experience. To streamline the customer experience insurance providers deliver, customer information needs to move seamlessly between touchpoints. That requires:

- A centralized customer data platform

- Shared interaction histories

- Connected support and digital systems

- Records every agent and touchpoint can access and update

The goal is to allow customers to switch channels without repeating information or starting over.

Personalize beyond the premium

Connected customer data creates opportunities beyond operational efficiency. However, many providers still limit personalized insurance to pricing and renewal discounts. Meanwhile, 72% of customers expect insurers to use their customer data to tailor offers and communications to their individual circumstances.

In many cases, you already have the information needed to make coverage feel more relevant:

- Renewal offers based on major life events

- Risk-prevention tips tailored to a policyholder’s property

- Safe-driving recommendations for auto insurance customers

- Health and wellness guidance aligned with coverage

Even small personalized experiences can have a measurable impact. Insurers that deliver more relevant experiences can achieve customer retention rates as high as 81%.

Tip: Before sending any personalized communication, ask a simple question: does this help the customer make a better decision, reduce risk, or get more value from their coverage? If not, it probably isn’t useful personalization.

Invest in proactive communication

Most customers would rather receive an update they don’t need than chase one they do. In fact, more than 80% of consumers want companies to reach out proactively when there is an issue, and 90% say it improves their perception of the brand.

In insurance, silence often creates more frustration than bad news. Timely updates reduce uncertainty, strengthen customer engagement, and prevent avoidable follow-up inquiries.

Start with high-impact communications such as:

- Automated claim status updates

- Renewal reminders at 90, 60, and 30 days

- Coverage change notifications

Tip: If customers have to contact you for a routine update, the communication arrived too late.

Train agents as CX specialists

Despite the rise of self-service, agents remain the highest-rated channel for customer satisfaction, particularly in life insurance. Some situations require more than speed and convenience. Customers seek reassurance, guidance, and clear answers from another person.

That’s why improving customer experience in insurance is impossible without well-trained people.

Beyond product knowledge, agents should be trained in:

- Active listening

- Empathy during claims conversations

- De-escalation techniques

- Clear, jargon-free communication

In customer-centric organizations, these skills carry the same weight as compliance, underwriting, and product training.

Measure what actually drives customer loyalty

Every improvement should connect back to a measurable outcome. Otherwise, it’s difficult to know what’s working and where customers still encounter friction.

The challenge is choosing metrics that reveal what customers are actually experiencing, not just how the business is performing.

How do you measure customer experience in insurance?

The most effective measurement frameworks combine several indicators that focus on customer behavior and help predict retention, customer lifetime value, and increased customer satisfaction.

Useful metrics include:

- NPS (Net Promoter Score): Used by 43% of insurers, NPS tracks customer loyalty over time. However, it doesn’t explain which interaction influenced a customer’s decision to stay or leave.

- CES (Customer Effort Score): CES measures how easy it is for policyholders to complete a task. It’s particularly useful for evaluating claims and onboarding experiences, where unnecessary effort often drives switching behavior.

- CSAT (Customer Satisfaction Score): CSAT captures feedback after a specific interaction. It works well for assessing claim updates, support conversations, and renewal discussions.

- Policy Comprehension Rate: This metric measures whether policyholders understand their coverage after 30, 60, and 90 days. Low scores often signal future cancellation risk.

- Churn by Touchpoint: This metric links customer departures to their last significant interaction. It helps teams identify where to enhance customer experiences most effectively.

Insurance customer experience trends shaping the industry in 2026

The fundamentals of insurance CX haven’t changed much. Customers still value convenience, transparency, and support. What is changing is how insurers deliver those experiences. Across markets, a few clear trends are beginning to define the next phase of customer experience in insurance.

The hybrid trust model (AI + human)

Automation continues to advance, but customers still value human support when situations become complex or emotionally charged. As a result, many insurers are adopting hybrid models that combine AI-powered assistance with human expertise.

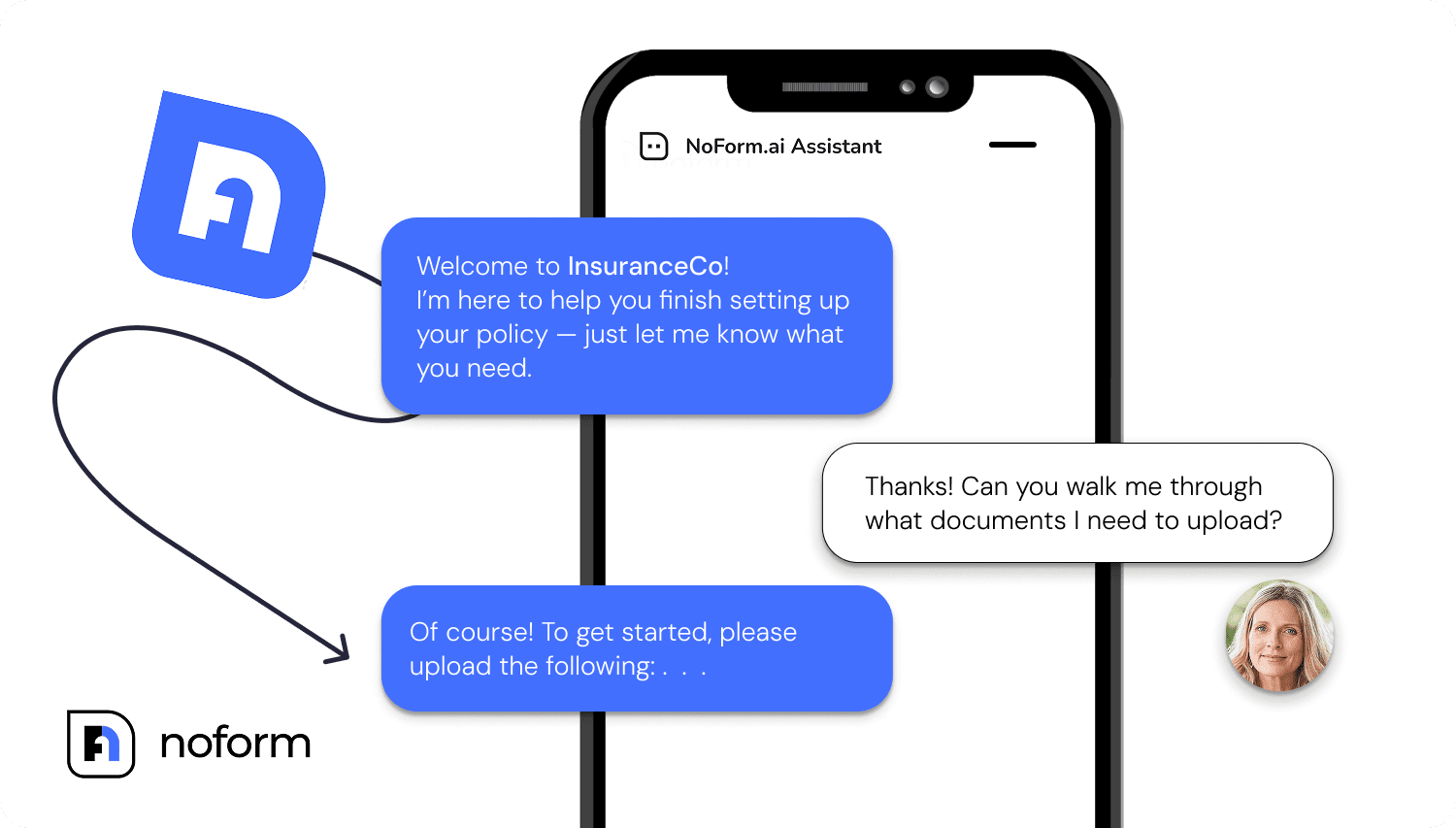

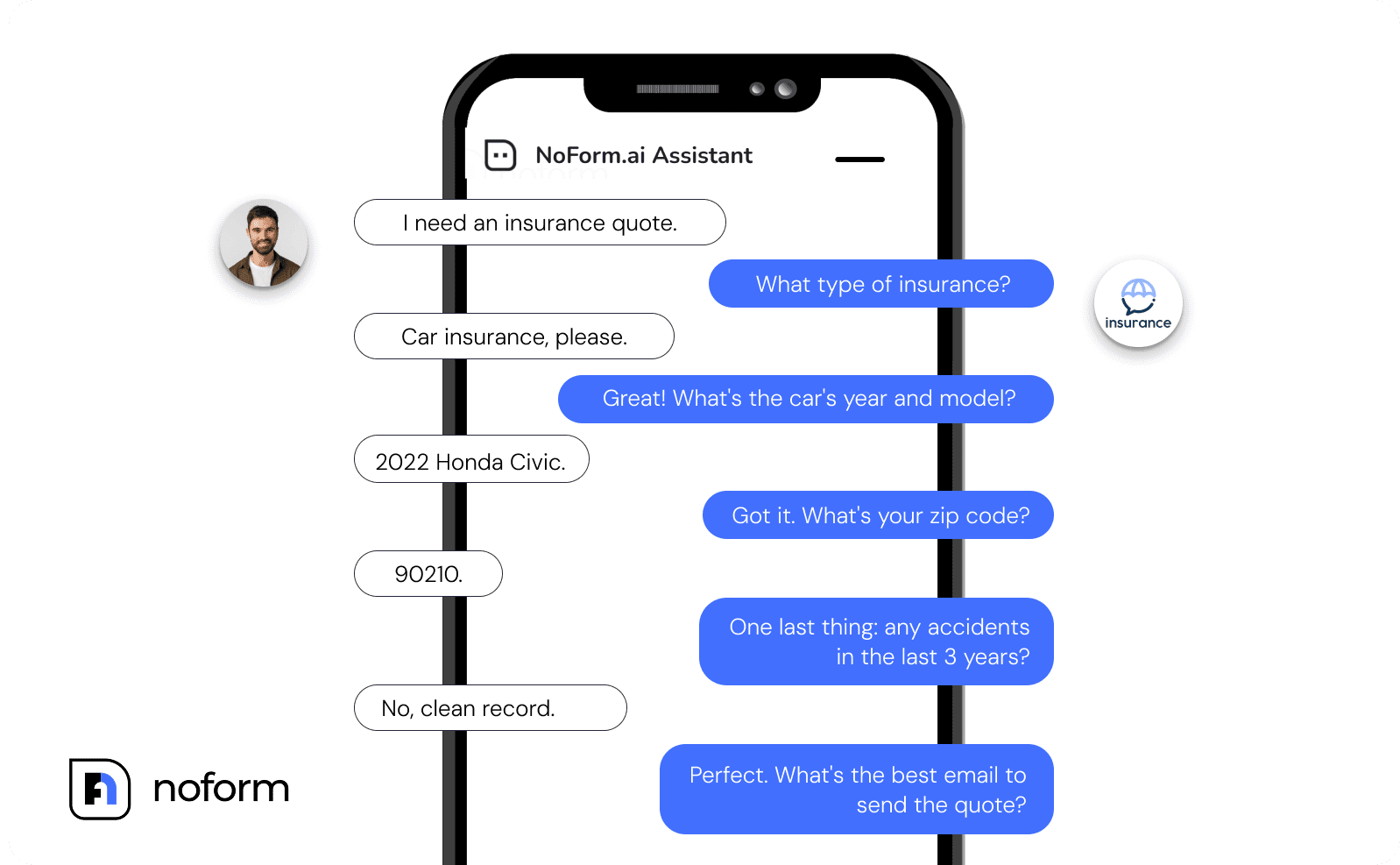

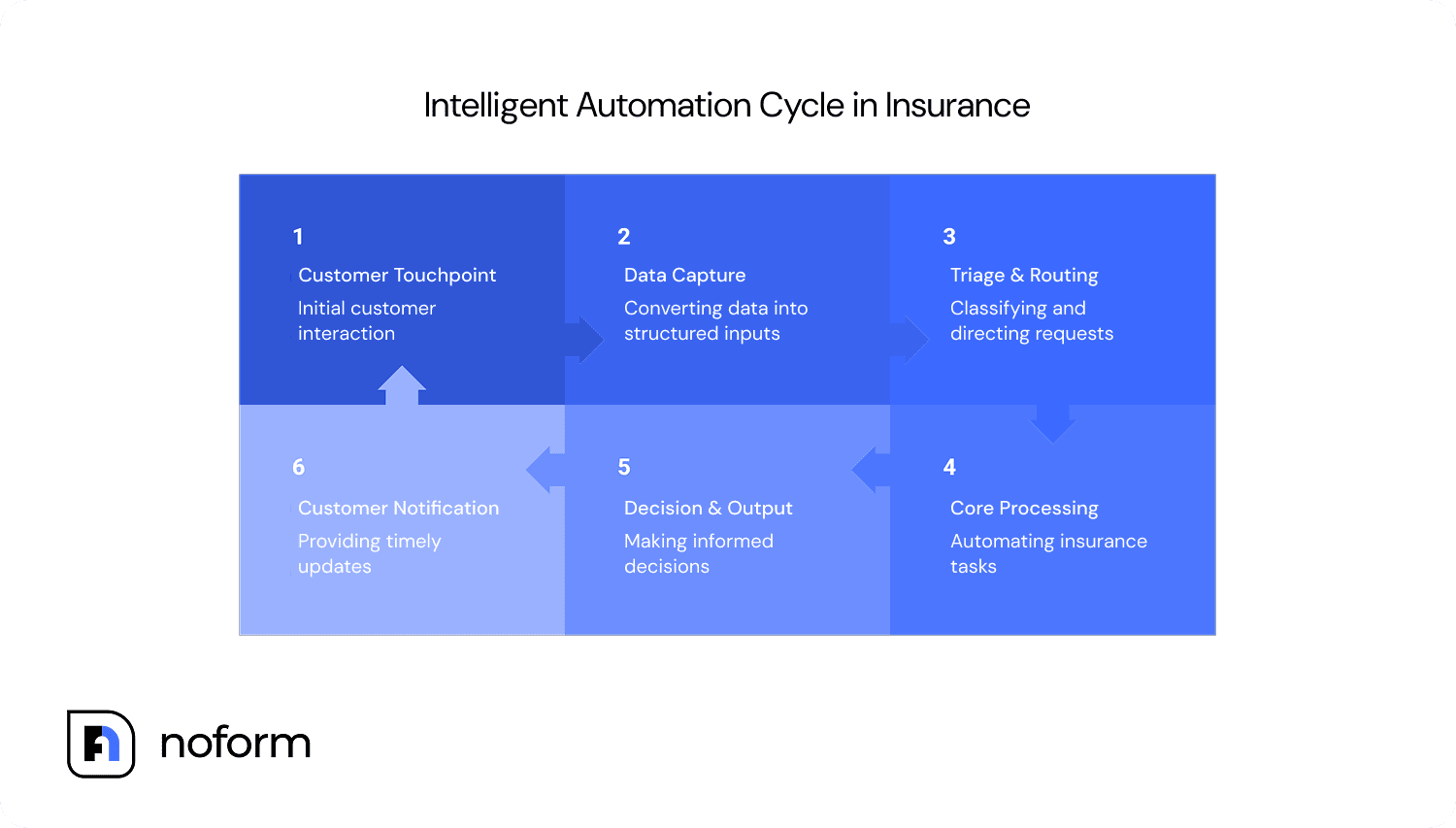

AI chatbots are a form of intelligent insurance automation that helps customers complete common insurance tasks through a simple conversation. Much like a human insurance agent, the chatbot asks questions, gathers information, and guides customers through the next steps in real time.

Rather than relying on a single chatbot, insurers can create and train multiple AI assistants with different responsibilities, placing them at specific stages of the customer journey from quote collection and coverage questions to claims support and document tracking.

As AI chatbots take over routine conversations, agents can dedicate more time to interactions that require expertise, empathy, and trust.

Tip: Use a no-code AI chatbot platform like NoForm AI and learn how to create a chatbot easily in our guide.

Embedded insurance

Another trend reshaping insurance CX is embedded insurance — coverage offered as part of another product or service, such as travel insurance during flight booking or device protection at online checkout.

In fact, 94% of insurers view embedded insurance as strategically important.

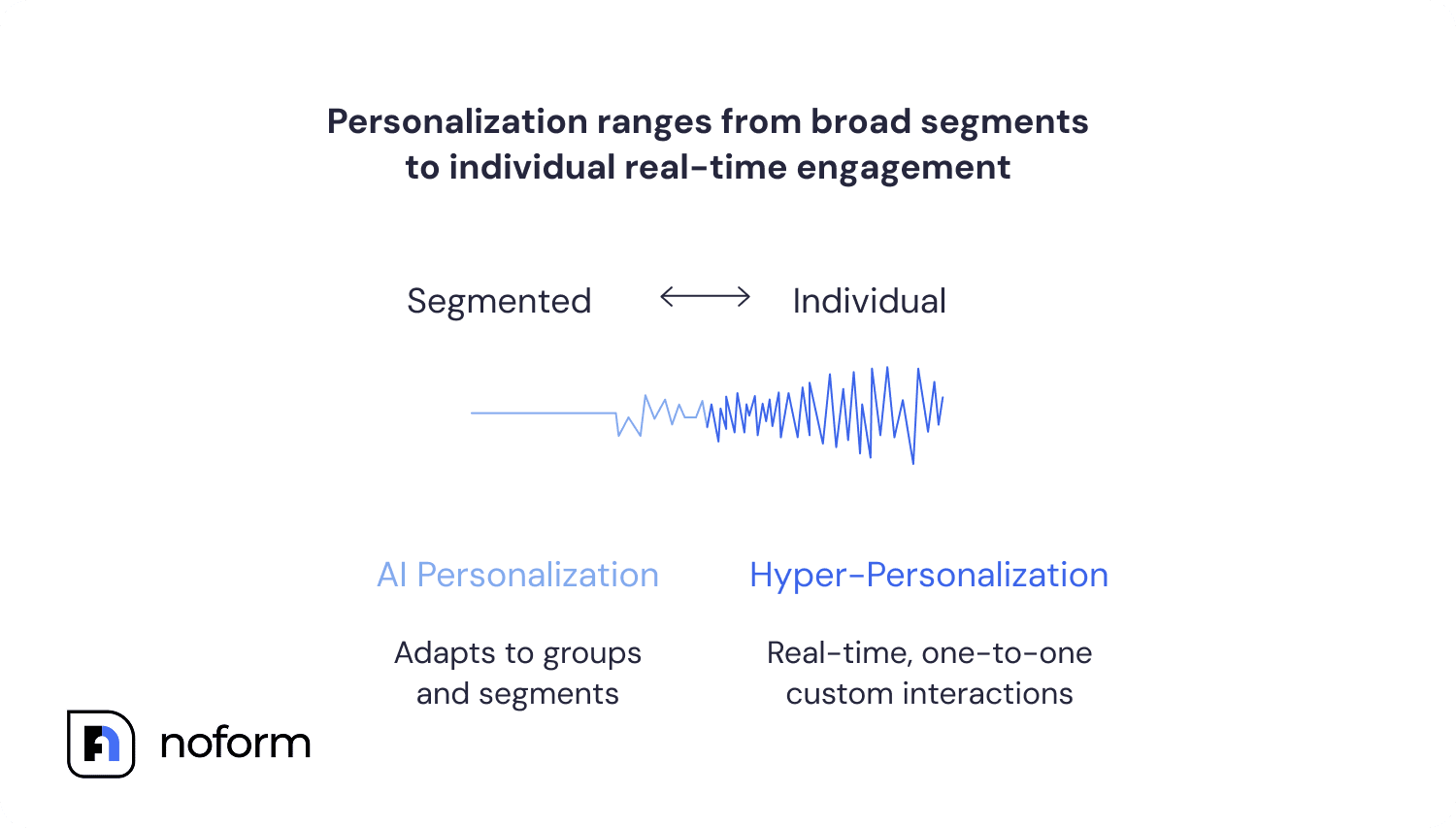

Hyper-personalization

Personalization has been part of insurance CX for years. Traditionally, that meant tailoring communications, offers, or recommendations to broad customer groups. Hyper-personalization takes it a step further by using real-time data and individual risk factors to adapt coverage, pricing, and customer experiences at the individual level.

For example:

- Pay-per-mile auto insurance based on actual vehicle usage

- Usage-based home insurance discounts tied to smart home devices and risk-prevention measures

- Coverage recommendations that adjust based on major life changes, such as marriage, relocation, or the birth of a child

The trend reflects a shift away from one-size-fits-all policies and toward insurance products that better reflect how people actually live, drive, and manage risk.

Omnichannel claims

Like personalization, omnichannel claims are not a new concept. What’s changing is the extent to which customers expect them.

Many providers are still struggling to meet that expectation. While 60% of U.S. insurance consumers say consistent cross-channel experiences increase trust, only 55% feel their insurer communicates through their preferred channel. Meanwhile, 65–70% of policyholders switch channels during their journey, and around 65% are likely to abandon an interaction if it becomes too repetitive or difficult to navigate.

Tip: The gap between what customers expect and what many insurers currently deliver remains significant. Organizations that make channel-switching effortless have an opportunity to stand out in an increasingly competitive market.

Conclusion

That’s why the five emotional touchpoints framework matters: it highlights where friction appears, where trust is built, and where the customer experience ultimately succeeds or fails.

Customer expectations aren’t slowing down. To meet them without increasing your team’s workload, book a demo or try NoForm AI to build an insurance AI assistant that can qualify leads, answer questions, and support policyholders 24/7.

Frequently Asked Questions

What is customer experience in insurance?

Customer experience in insurance covers every interaction a policyholder has with their insurer, from getting a quote and buying coverage to managing a policy, contacting support, and filing a claim. Unlike retail or banking, insurance CX runs on low frequency and high stakes. Most policyholders go a full year without contacting their insurer, then call during a car accident, a medical emergency, or a property loss. That one interaction carries more weight than years of quiet service.

What do insurance customers want most from their insurer?

Insurance customers prioritize fast, transparent claims handling. J.D. Power data shows 80% of auto policyholders who had a poor claims experience have switched insurers or plan to. Coverage and pricing drive the initial purchase. A slow or opaque claims process is what ends the relationship.

What role does AI play in insurance customer experience?

AI handles routine policyholder tasks at scale, including coverage questions, claim status checks, and document submissions, so human agents can focus on complex and emotionally charged situations. Insurers using hybrid AI-plus-human models see higher retention rates than those running either alone. AI tools that can’t access complete customer histories still fragment the experience regardless of capability, so integration quality determines the outcome more than the technology itself.

Why do insurers struggle to improve customer experience?

Disconnected legacy systems are the core obstacle. When customer data doesn’t travel between channels, agents ask repeat questions, updates get lost, and policyholders experience the insurer as fragmented. McKinsey identifies core system modernization as the industry’s top operational challenge. 60% of insurers also report having no clear CX strategy, which means technology investments fix isolated problems without improving the end-to-end experience.

What metrics should insurers use to measure customer experience?

Customer Effort Score at claims and onboarding, churn rate by last touchpoint, and policy comprehension rates at 30, 60, and 90 days are the most predictive retention metrics. NPS, used by 43% of insurers, tracks loyalty trends but won’t tell you which interaction triggered a cancellation. CSAT after claims updates and renewal conversations adds transaction-level precision.